Welcome to Family Money Plan!

We Help You Get Better With Money.

We’re dedicated to helping busy parents, who are stressed out about money, find their way out of the mess, by providing them easy action steps so that they can create a life they love.

Getting Started is Easy!

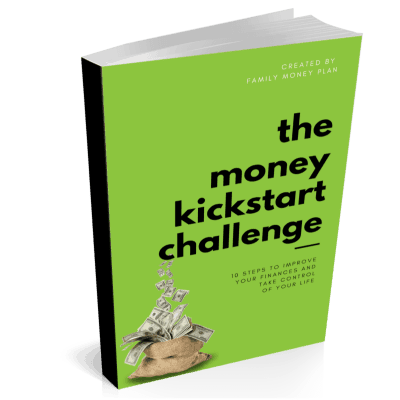

Take the Free Money Kickstart Challenge, it’s what we did to revolutionize our money.

Family Money Plan

We Help You Get Better With Money.

We’re dedicated to helping busy parents, who are stressed out about money, find their way out of the mess, by providing them easy action steps so that they can create a life they love.

We Help You Get Better With Money.

We’re dedicated to helping busy parents, who are stressed out about money, find their way out of the mess, by providing them easy action steps so that they can create a life they love.

Welcome to Family Money Plan

Helping Parents Thrive!

We are here to help you master your money so you can create the life you love.

As Featured In:

First Time To Family Money Plan?

Find Out What We Are All About Here.

⬇️

I Want To Find Out About:

Wondering where to start?

Take Our Free Email Course On How To Manage Your Money. It’s the same system we used to get out of debt and become mortgage free quickly.

Check Out The Latest Posts

Check Out The Latest Posts