Hello!

Imagine this: It’s a few years from now, you drive into work , this is your last day. Some time ago you decided to take control of your money. Since then you have been handling your money properly. You haven’t stressed about money in years because you found a system that worked for you.

Because of this new found control, you are able to retire without worry. You have finally found your FREEDOM!

Today we are going to talk about saving money. More specifically saving money for retirement, or at the very least FREEDOM!

Let’s Get F.I.R.E. – Financially Independent and Retire Early

In the personal finance community the word is F.I.R.E (Financially Independent, Retire Early).

What it means is having enough income from your investments so that you are able to leave your job and do what you truly love to do (assuming you aren’t doing that already).

This account is all about the ability to quit your job once you have enough money saved up.

This should be your long-term goal. To achieve financial independence so that you can retire early.

The Biggest Mistake People Make With Their Budget

Whenever someone tries to budget, they start trying to figure out their spending and their costs and start cutting expenses. Costs are important, but it’s better to take a long-term focus and put first things first. With the focus on cost cutting the give very little attention to how much they save.

Most commonly I hear: “I’ll save whatever is left at the end of the month.”

I’ve been guilty of this too.

It sounds great, but if you were like me, there was never anything left at the end of the month.

*GULP*

In fact, there was usually more month at the end of the money.

*DOUBLE GULP*

Your future freedom is all about getting yourself set up for the long-term. Which is why you need to make saving your first priority.

From now on “Pay Yourself First” should be your mantra.

How Much Should I Save? Minimum 10%

Go through many of the personal finance books and you will read that you should always save 10% of what you make. When I started working in the “real world” I preferred 10%. I felt good that I was putting some money away every pay check.

Then when I got into personal finance I did some math and found a scary truth:

10% is not enough in many cases

A Different Way To Look At Savings

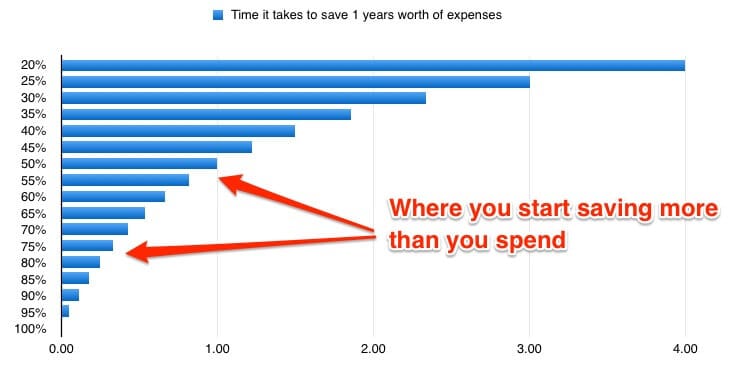

With F.I.R.E in mind consider this: If you save 10% then it takes 9 years to save up 1 years worth of expenses.

Or to look at it another way, if you save 10% for 9 years, you can live the 10th year for free.

That sucks. I mean it’s better than nothing, but still…

Here’s why; saving 10% means out of 40 working years you will have saved 4.5 years or so of Freedom (not including investment returns, inflation and a bunch of other things).

It’s just not enough.

When you look at how much you should save everyone has a different idea.

Here’s How I Look At It

I like to think of things like this: If you make $10,000 a year and save 20%, then you live off $8000. Which means you save $2000 a year.

After 4 years, you have saved up enough for 1 year of expenses.

The more you increase that savings amount the quicker you save.

Here is what it takes to save up for 1 year of expenses:

How many years to save 1 years worth of expenses

The F.I.R.E. Account

This account is where you pay yourself first. You will be putting a percentage of your pay into it every time you get paid.

EVERY. TIME. YOU. GET. PAID.

What Do I Use This Money For?

This money is used to fund your F.I.R.E. (i.e. Freedom/Retirement/Walk Away From Work). You are growing this account so that you can use the money to fund your retirement.

What to do with the F.I.R.E. Account

This account is for growing your nest egg. You want to grow this nest egg so big that you can live off the residual income it provides.

How Do I Do This?

The simplest explanation to grow your money is to invest. Investing is outside the scope of this course but I’ll give you a quick overview of the two types on investments I usually consider.

Asset Growth

Investing in assets that will grow in value. (Like Stocks, Businesses, Bonds, Land, Real Estate etc…) Anything that can increase in value over time so eventually you can sell it for more money than you paid for it.

Passive Income

Passive income is when you own something that pays you a residual for owning it. If you are new to the idea of passive income and want to learn more about what passive income is you can read this article.

Some passive income ideas are:

Royalties from books, songs and other intellectual property

Rental Income from Real Estate

Investing In It’s Purest Form

Don’t be intimidate by investing. In the simplest terms: Investing is anything that you can do to get a return on your money greater than what you put in.

You Might Be Investing and Not Know It

Before you get worried about investing I will tell you a way I used to “Invest” without knowing it.

When I was younger, I had a job at a used music store. Part of this work had people coming in to find a good deal on a used guitar. To fill this need I would go out to people’s houses and pawn shops and look for musical instruments that I could resell. It was very common to find a guitar for $100 that I could easily sell for $200 or more within a few months, sometimes the same week.

Now this wasn’t “sophisticated” investing. But I was getting an amazing return on my money.

The Point Of The Story

There are tons of ways to grow your money, don’t be intimated by stocks or real estate. More importantly don’t feel like you need to invest in them if you don’t understand. As a rule never invest in something you don’t understand.

I have heard of people that go to thrift shops and buy vintage clothing then turn around and sell it on Ebay for 30 times what they paid for it.

The trick here is that you probably have knowledge of something you can leverage into some type of investment and get a return on your money.

Think outside the box.

If you already have investments and are looking for a way to look at all of them in one snapshot you should check out Personal Capital. With Personal Capital you are able to add all of your bank accounts, mortgages, investments, loans and credit cards. This will give you a great overall money tracker and expense overview. It’s also a great way to see how you money is growing over time.

Homework

Tonight’s homework is simple. Decide how much of your take-home income you want to save. Then decided how much you are going to start saving.

If you are starting at 10% trying raising it 1% a month until you get to your ideal number it may be easier than you realize.

I will see you tomorrow when we get into our living expenses.

Until then take care!