How a Mutual Fund Gets Paid

The Important Numbers

An Unpleasant Conversation With My Financial Advisor

Here Is The Conversation:

Now Comes My Patented: “Here’s the thing…”

“Here’s the thing Carl,” I started. “This fund hasn’t beaten the market. So why would I stick with this fund, or any other, when I can buy an ETF that matches the market on my own? Or if I don’t want to do it on my own, go with robo-advisor like Wealthsimple (which you can get a $50 sign up bonus as a reader) that only charges me 0.5% to manage and invest my money.”

Carl: “That is quite a bit lower, honestly the fund you are in is too high. Which is why we are wanting to get you out of it. But we need to get paid too, which is why there is the 2% fee.” Carl said.

Side note: Honestly I sympathize with Carl, he’s a good guy. He has mouths to feed and the rules have changed and I can tell this isn’t the first time he’s had this conversation this week.

“I get that Carl, but it’s my money and that 2% difference adds up quickly. I’m sorry I’m going to need to switch. Cash me out”

What’s In A Percentage?

Taking a quick glance at Wealthsimple’s fee chart, they charge 0.5% on a portfolio under $100,000. In switching to Wealthsimple, the $30,000 that I have invested would cost me $150 in fees a year, not the $900 I just paid.

Under Carl’s new fee of 2% I would still pay an extra $450 over the 0.50% with Wealthsimple.

Over the next 10 years, that’s $4,500 of savings in fees alone from switching to Wealthsimple. Like I mentioned It adds up.

What Are My Options Now That I Have My Funds?

I have a few options. I can switch to Wealthsimple, manage my own funds through ETFs with Questrade, or switch to another fee only manager.

For right now I’m doing the first two. I like my dividend strategy, but I also want to have some money in the whole market. Wealthsimple makes it super easy to do this when I don’t have time to research stocks so I like the balance I have.

Related Post: Open an Account With Wealthsimple and Get a $50 Sign Up Bonus

Should You Fire Your Financial Advisor?

Honestly, I have no clue. For me to be as brazen to say fire your financial advisor would be terrible advice. Your situation is unique and what makes sense to my situation may not make any sense to yours.

The answer of course is: It depends on your situation.

What I do know is that if you are paying fees of any kind you should be aware of them. Those fees should get you something over and above investing in a under performing mutual fund like I was in.

Your money is important to you, and it should matter to the person managing your money too.

As for me, I’m sure this isn’t the last time I will have someone else manage my funds. For right now, Carl’s new fund fell into the “I can do this myself” part of the equation.

A Couple Of Takeaway Points

Don’t think of percentages as pennies that are easily discarded. Think of it as the actual amount, and what that means. Yes 3% on $100 is on $3, but over time that adds up. Small amounts count and not giving the small amounts the proper respect tunes you out to your money.

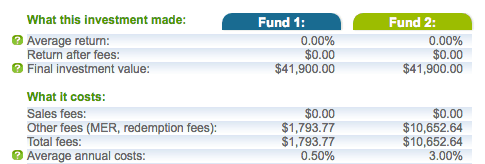

The small amounts are what make up bigger amounts. Want proof? Here’s how much I would save in by switching to Wealthsimple.

This is just based on fees. Wealthsimple is Fund 1 and my old mutual fund is Fund 2. Take a look at the second last line “Total Fees”

That’s $8,858.87 in fees I’m saving in 10 years based on nothing but a simple switch. I basically just saved the equivalent of a second trip to Disney.

Money doesn’t need to be all about huge sweeping changes, sometimes the small initial saving can add up to bigger things. In this case a small change will make a very big deal over the years.

What do you think? Should I have stuck with my advisor or am I right for going out on my own?

I fired my financial advisor too. I couldn’t figure out what value he and his firm added and the cost was substantial when you added it all together. https://racingtowardretirement.blogspot.com/2017/02/how-to-lose-money-on-your-investments.html

I’m a Wealthsimple client. Left RBC DS in spring 2015 after drilling down and discovering some of my funds had MERs close to 3%. I realized someone was driving a way better car than me, that I was paying for, lol. When I had the conversation described in this article with *my* advisor, she was rude and implied that I didn’t know what I was talking about and should be grateful for the work she and RBC DS did on my behalf. Um, buh-bye.

Wealthsimple recently teamed up with Priority Pass. So now, when I travel using all the money I’m saving on fees, I get to sit in a nice lounge while I await my flight. Sweeeet.

Hey Sue!

That’s awesome about the priority pass. I didn’t know that. Yeah those MER will slowly suck you dry if you don’t pay attention to them. Way to go making the switch!

Thanks for sharing. Learned something there that I should do my due diligence and start paying more attention to MER fees.

Hey Jordan! Yeah those fees can really start to do damage as your portfolio grows, it’s kind of crazy!